What do Kraft Mac N’ Cheese’s latest launch and Pepsi’s Poppi purchase have in common? They’re both attempts by major CPGs to reclaim food dollars that, for years, have drifted toward private label and emerging challenger brands.

Private label has steadily improved its perceived quality perception and price matrix, transforming into a formidable opponent to legacy brands. U.S. sales hit $330 billion for the segment in 2025, representing 24% share of the F&B market by value, per Circana data.

Today’s multiples augurs continued domestic growth. Mature markets, such as Australia, where private label accounts for 40%-unit share hint that tomorrow’s aisles will boast more store brand selections.

As private label exceeds the “quarter of the market” benchmark, national brands are challenged to refine their value proposition.

“The traditional model, where brands achieved ‘staple’ status through long on-shelf presence and blockbuster marketing budgets, has been completely disrupted,” Guy White, CEO and founder of Catalyx, told FI in the recent State of the Consumer report.

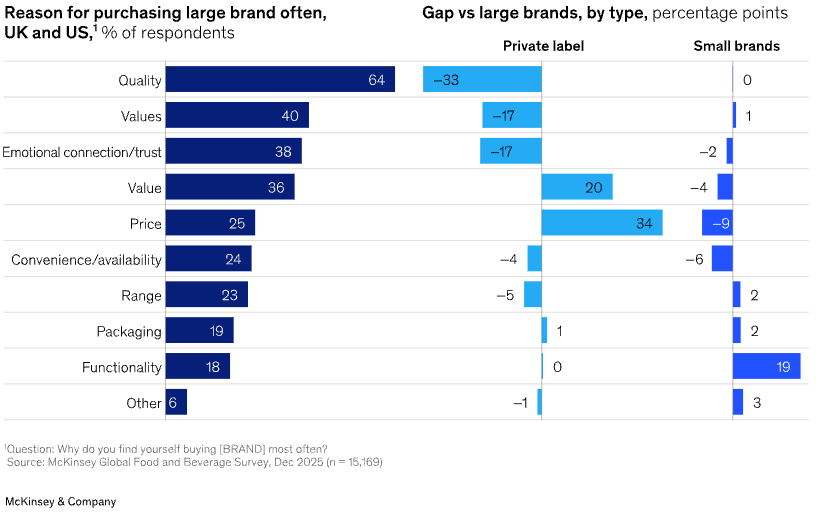

Staple goods now come in many shapes and sizes. Recent McKinsey & Company data corroborates this shift. While large brands still lead on perceived quality, they’re steadily losing share to private label and challenger brands on value, trust, and functionality.

In this new environment, consumers tend to turn to challengers for discovery and private label for affordability. CPG giants’ household penetration, meanwhile, gradually erodes.

Nationals Bet on Affordable Luxury

Smart legacy leaders, however, are countering these pressures by targeting portfolio vulnerabilities with strategic acquisitions or investing in innovation strategies.

Kraft, for example, is going toe-to-toe with better-for-you premium brand Goodles with its Restaurant Edition lineup.

Recent additions include Parmesan Pesto, Romano Cacio e Pepe, and Monterey Jack Caramelized Onion, with an emphasis on functionality, indulgence, and affordability. Each offering boasts $1 per serving and 10g of protein. Kraft, like many national brands, is looking to win with product.

Consumer trust remains one area where major brands retain an edge. A recent Circana report found that four percentage points more consumers “completely trust” them compared to store brands. This is significant considering 80% of shoppers believe it’s important to buy a brand they trust.

This is largely why the current market is particularly kind to CPG M&A activity. PepsiCo’s bet on Poppi is one clear example of bringing a breakout “modern soda” to the everyday shopper. The strategy involves acquiring fast-growing challengers offering the “affordable luxury” they haven’t quite worked out for themselves, then scaling them through their established networks.

M&A plays represent tried-and-true playbook for national brands. In 2022, Keurig Dr. Pepper took minority stakes in emerging brand C4, iterating the move again in 2025 with Bloom to capture some of the long-term growth happening in the functional beverage subcategory, an area where its portfolio comparatively struggles.

The road ahead may be arduous for national brands, but the right strategies of today will beget growth opportunities down the road.

“CPG leaders must sharpen how brands win with consumers, rebuild the pipeline of new buyers, and unlock the next wave of productivity to fund reinvestment and sustain growth,” McKinsey wrote in its report.

Private Label’s Angle

Consumers want cheap items. Enter private label.

FI previously covered the trade-down phenomenon as it related to Gen Z patterns, but research indicates it is generation agnostic. Across the board, more than 55% of consumers agree that they seek out cheaper alternatives on staple purchases.

These shifts are made possible because of private label brands’ ability to rise to meet consumer needs. Retailers are responding with heavy investments in their own brand portfolios.

Walmart, for example, recently revamped its private label Great Value packaging to consistently showcase nutrition and benefit claims as it prepares to remove synthetic dyes from its private label brands by 2027.

The redesign uses brighter colors and cohesive visual branding to emphasize both health attributes and experiential eating. These modifications prove that store brands are no longer content to compete on price alone.

The new value standard for food and beverage purchases dictates that budget, better-for-you, and experiential offerings will continue to gain ground as consumers think critically about each item they purchase.

The new value standard for food and beverage purchases dictates that budget, better-for-you, and experiential offerings will continue to gain ground as consumers think critically about each item they purchase.

In this battleground, private label, and, more specifically, premium private label is moving into specialty categories and support, at a better price point. Walmart’s Bettergoods and Target’s Good & Gather Signature are two clear strategies to claim this emerging space.

It helps that consumers no longer turn their nose at generic brands. In an era where Trader Joe’s and Aldi’s own brand selections are evangelized, the scales have tipped in favor of retail brands as cultural engines.

The data characterizes this grocery cart recalibration: private label is becoming a beloved choice in terms of quality, value, and selection. The McKinsey report that U.S. consumers value it similarly to mature markets such as Japan and Europe. As a result, 34% of domestic respondents say they’re spending more on these items than before.

The Food Institute Podcast

In this episode of Food for Thought Leadership, Food Institute Chief Content Officer Kelly Beaton steps in as guest host to interview Fransmart CEO Dan Rowe on the evolving restaurant labor market. Rowe challenges operators to view labor not as a cost to minimize but as a strategic investment, noting that the most successful brands are those that “staff for the sales they want” and prioritize retention, engagement, and culture amid ongoing workforce constraints.