For consumer products companies, including those within the food and beverage industry, deal activity expectations were high in 2025. Results, however, were not so positive.

Deal activity never found its footing last year, finishing at its lowest level since 2020 and well below market forecasts; however, sentiment is beginning to turn. As firms look ahead to 2026, we are seeing signs of re-engagement that could mark a pivot away from the caution that defined much of the past year.

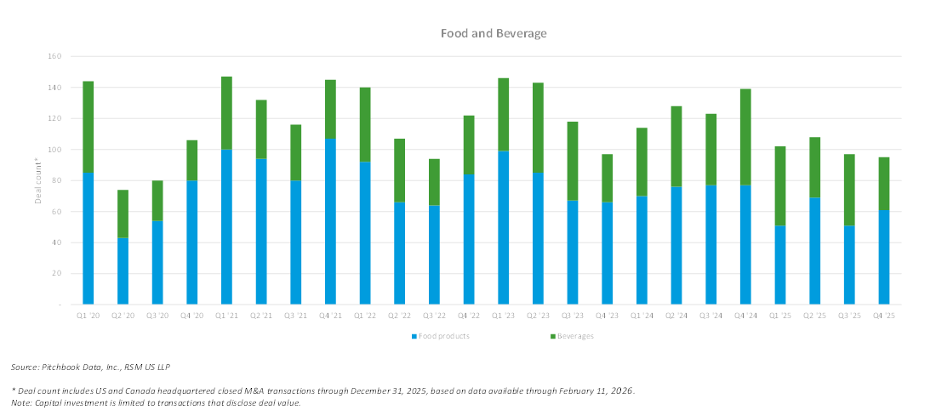

Deal volumes were negatively impacted throughout 2025 by uncertainty around tariffs and other regulatory policies, weakening consumer purchasing power (as evidenced by continued lower retail sales in December), and indicators of a softening labor market. Despite several mega transactions, including Mars’ acquisition of Kellanova in December, the middle market mergers and acquisitions rebound remained out of reach.

From Stalled Momentum to Cautious Re‑engagement

Financial sponsors are expecting to capitalize on recent (and expected future) interest rate cuts through increased deal activity, following a year of cautiously navigating a higher interest rate environment. Meanwhile, strategics are reshaping their portfolios through strategic acquisitions and divestitures in response to slower growth, margin compression and activist shareholders, following a two-year slowdown in corporate M&A.

Moreover, the debt that funded the post-pandemic flurry of deals from late 2020 throughout 2022 is beginning to mature, which we believe will be another catalyst for both increased deal volumes and elevated refinancing activity. This will likely be the year where the hope for significantly improved performance is overtaken by the reality of the need to realize lower than hoped returns as limited partners look for liquidity from aging portfolios. Given these factors, we continue to see elevated execution risk, as buyers and sellers have difficulty aligning growth assumptions, which often result in increased reliance on pro forma adjustments and earn-outs driving an unbridgeable valuation gap.

We expect many themes from the last two years to remain into 2026, most notably a continued focus on add-on acquisitions. This trend has driven explosive growth within home services (home improvements and renovation, personal wellness and services) and consumer services (primarily wellness, medical and automotive) as Baby Boomers look to exit businesses started decades ago. We are beginning to see investors shift dollars toward commercial businesses with higher barriers to entry and stickier customer bases. (Note: activity within this sector is not fully reflected in consumer products deal counts given inconsistency in reporting.)

We expect corporate activity to accelerate into 2026 as organic growth stagnates and strategic acquirers look to the deal market to plug gaps in portfolios.

The Continued Breakup of Big Food Drives Strategic Opportunity

The overriding theme to emerge in 2025, which we expect to continue in the coming years, is the continued breakup of Big Food. After more than a decade of consolidation of smaller brands that struggled to grow with shifting consumer tastes and trends, Big Food is starting to divest brands as they redefine core portfolios to align with changes in consumer behaviors with a higher emphasis on protein and clean ingredients.

While the recent announcement that Kraft Heinz will shelve its proposed split has tempered this trend, many other Big Food companies have taken steps to separate brand categories, either because of investor demands or shifting strategies. We expect this to shift focus from creating standalone entities, which brings its own related complications and execution risk, to more surgical structures that better enable well-placed buyers to more easily and confidently absorb these brands. Sellers that build confidence in a clear roadmap for operational and financial entanglements will perform better in this environment.

This emphasis will put renewed focus on post-acquisition strategies to drive value-creation opportunities and allow for sharper focus and faster decision making.

The catalyst for anticipated deal activity in 2026 and beyond is the continued breakup of Big Food, driven by shifting consumer preferences, activist investors and stagnant organic growth. Additionally, pricing appears to have reached a ceiling with consumers and in some cases reversing, resulting in many food and beverage companies who continue to be challenged by elevated input costs to look for smaller brands in order to generate scale, or consider divesting brands more exposed to commodity fluctuations.

K‑Shaped Consumer Economy Creates Divergent M&A Winners

We expect the K-shaped economy to continue into 2026, as growth is realized across both high-end brands at premium prices and value- or private-label brands appeal to a wide variety of consumers. While the expansion of GLP-1 usage has driven a reduction in overall food consumption, consumers have reallocated wallet share toward higher-priced premium, better-for-you, or other products with enhanced health benefits, driving increased sales volumes and valuations for premium brands despite years of inflation. Non-alcoholic beverage deals continue to gain traction from this consumer subset.

At the same time, many food and beverage companies are capitalizing on cost-conscious consumers shifting toward value or private-label brands in the wake of record inflation levels in recent years. Companies have expanded investment in private label brands, realigned product packaging to fit a variety of price points, and in many cases incentivizing consumers through promotions or more permanent price reductions. This environment will continue to benefit manufacturers of private-label products and branded products that can demonstrate value.

Looking forward

While challenges remain, improving sentiment, portfolio reshaping and maturing capital structures are expected to bring renewed momentum to food and beverage deal activity. Further, as evidenced by commentary from many Big Food companies who participated in the 2026 Consumer Analyst Group of New York annual conference (CAGNY), businesses that focus on functional nutrition, have strong consumer connectivity and are driving performance through AI enablement will receive continued investment interest. In addition, companies that move early, align expectations and plan for execution will be best positioned to turn uncertainty into opportunity.

Portions of this article appeared in RSM US LLP’s The Real Economy blog: Consumer products M&A update: Recovery in sight?.